MANHATTAN — Many New Yorkers often rack their brains over the question of whether to buy or rent.

Well, the data crunchers at real estate search engine StreetEasy believe they have the answer: It makes financial sense to consider owning if you plan to stay in the city for more than 5 years (and have the down payment to do so).

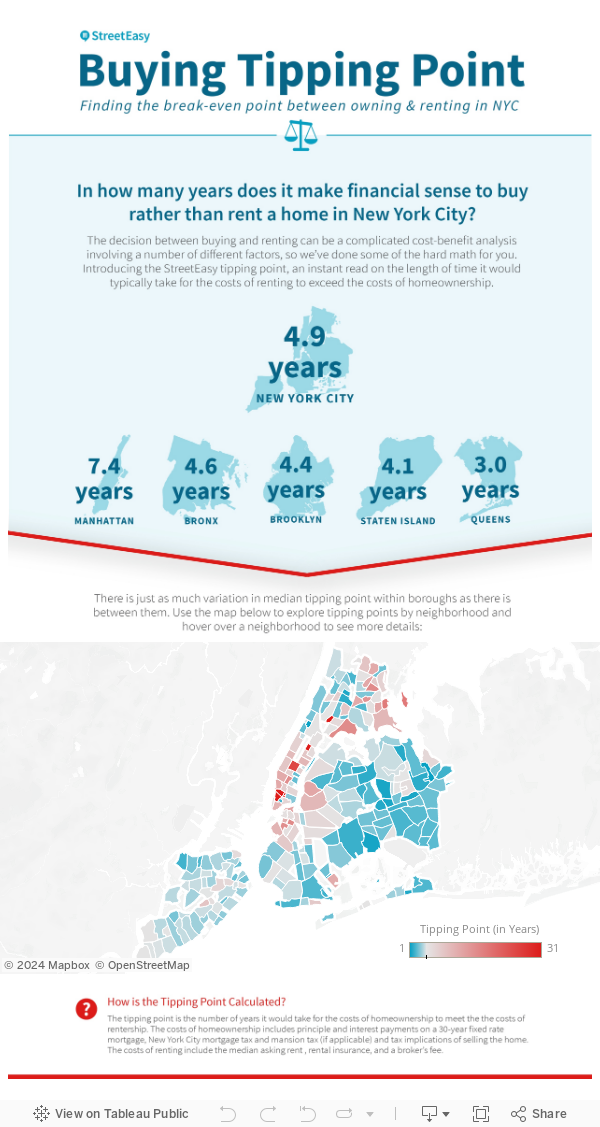

That was the median “tipping point” citywide where renting a home would exceed the costs of buying a “comparable” home, according to the Streeteasy report released Monday.

“Homeownership makes financial sense in New York City much sooner than most might imagine,” StreetEasy data scientist Alan Lightfeldt said. “Although it takes roughly three years longer in New York City than elsewhere in the country, homeownership makes sense in less time than is often said it takes to become a ‘true New Yorker’” — which is often said to be 8 years, he noted.

The greater the tipping point, the longer a resident would need to stay in a home for it to make financial sense to buy rather than rent — and different neighborhoods saw a range of tipping points.

Of all the nearly 300 neighborhoods tracked in StreetEasy’s analysis, the ones with the quickest payback included West Harlem at 1.2 years (where the median sales price was about $199,500 and the median rent was $2,200 a month) and Roosevelt Island at 1.4 years (where the median sales price was $398,746 and median rent was $3,199 a month).

The majority of the quick payback neighborhoods were in Queens: Howard Beach (1.4 year), Briarwood (1.4 years) and Alley Park (1.1 years).

The majority of the areas where the payback was longest were in tony Manhattan neighborhoods, including TriBeCa, Carnegie Hill, NoLiTa and SoHo, which all had a median tipping point of more than 31 years — meaning that homeowners would end up repaying their 30-year fixed-rate mortgage before ever reaching the tipping point.

But The Bronx was home to the second largest share of neighborhoods. In the South Bronx neighborhood of Melrose, for instance, the tipping point was also more than 31 years.

But Melrose's long tipping point was for reasons very different from the pricey Manhattan areas.

“Home value appreciation could be very low in an area which lessens the chief benefit of ownership. This is the case with Melrose,” Lightfeldt said. “Second, the net costs of owning may be so high in a neighborhood that it pushes out the tipping point. This is the case of SoHo, TriBeCa, and other Manhattan neighborhoods with a high tipping point, where sale prices are among the highest in the city.”

The StreetEasy analysis, looking at 2015 prices, included costs of homeownership, 30-year fixed-rate mortgage rates, property tax rates, purchase and selling costs, maintenance costs, renovation costs, homeowners insurance, capital gains tax rates, the city mortgage tax and the mansion tax, where applicable.

But some brokers warn would-be buyers from taking such simple calculations at face value.

"I rent in New York City and bought real property outside of the city," said Karla Saladino, of Mirador Real Estate. "I personally have been finding the housing market in New York City inflated."

When young, single New Yorkers are looking to buy "starter" apartments, but might want to rent it out since they aren't sure how long they'll stay, she cautioned them that their condos or co-ops might change rental rules, for instance.

"If you're buying and think you'll outgrow it and rent it out and don't plan on being involved with that board — for me, I was not super-comfortable with that," she said.

Even if you are planning on staying for the long term and becoming a part of the board and your building's community, Saladino said there might always be unanticipated events, like pricey assessments for roof work, or the loss of a job that make payments cost prohibitive.

"It's a lot of money down and you're not liquid anymore," she said of buying. "And you are signing a document that you owe a certain payment every month for 30 years."